How Does Penn State’s Self-Funded Healthcare Plan Work?

It’s important to understand your health plan because your choice may have many different financial and health care consequences for you and your dependents. Health insurance has traditionally been a way for a group of people to pool their money so that individuals who accrue medical expenses — in particular, expenses related to catastrophic medical claims — can pay for them using funds from the pool of money. With this system, some people may need to tap into the fund frequently, while others may not ever use it.

Health insurance began in the United States as a way for people to purchase coverage for hospital care in the event they would need to be hospitalized at a later date. After that, medical insurance expanded to cover the costs of other medical services, such as doctor appointments and laboratory testing, and eventually it became a benefit that was offered to employees by their employer.

Employer-sponsored plans, as opposed to individual plans, make sense because there are more people to contribute to the pool of money than with individual plans. In addition, when the workforce is diverse, the risk pool can also be diverse, meaning that it may contain a mix of healthy and ill individuals, which keeps costs in check.

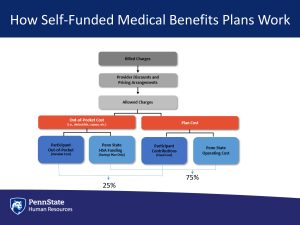

Smaller employers typically buy into fully-insured plans, where premiums are paid to an insurance company. Larger organizations, like Penn State, are frequently self-insured, meaning that the employer provides health benefits with its own funds, and with those funds, pays for the health claims submitted by the plan members. Under a self-funding arrangement, when medical claims in the insured population rise, the employer must pay more for the insurance. Self-funding allows for the employer to have more control over the plan design, however, and can lead to the creation of plans that are geared toward what the employee population wants and needs.

Penn State’s two health plans, the PPO Plan and the PPO Savings plans, are preferred-provider organizations (PPO), which means that the insurance company contracts with medical providers (physicians, hospitals, laboratories, allied health specialists) who agree to a negotiated fee that is generally lower than their standard fees. This negotiated fee appears as the “allowable charge” on a plan member’s Explanation of Benefits form, which is sent to the member following a visit to a provider.

Under a general PPO plan, the providers who agree to the negotiated fee structure are considered to be “in-network” providers. Any health plan member who obtains services from a network provider will have less out-of-pocket expense than if that member visited an out-of-network provider.

Find more detailed explanations on how the two plans work at the links below.

Each Plan’s Out-of-pocket Expenses

When choosing the health care plan that best meets the needs of employees, one consideration is out-of-pocket expenses. Learn how payroll or premium contributions, deductibles, coinsurance and copayments impact the cost of your plan.

How Each Plan Works

Once you’re familiar with the out-of-pocket expenses, you can track the path of cumulative (increasing) out-of-pocket expenses until they meet the total out-of-pocket maximum on color-coded graphics, and review scenarios below that explain how each expense is recorded for both individual and family plans, and applied to the total out-of-pocket maximum.

PPO Savings Plan – How it works

Determining your Risk Tolerance for health care spending

Factors to consider before choosing between the more predictable, but higher fixed-costs of the low-deductible PPO Plan, and the more variable costs of the PPO Savings plan.