“Beth” is the first of four Penn State employee examples illustrating claims and premium expenses that a Penn State employee could expect to pay within both plans.

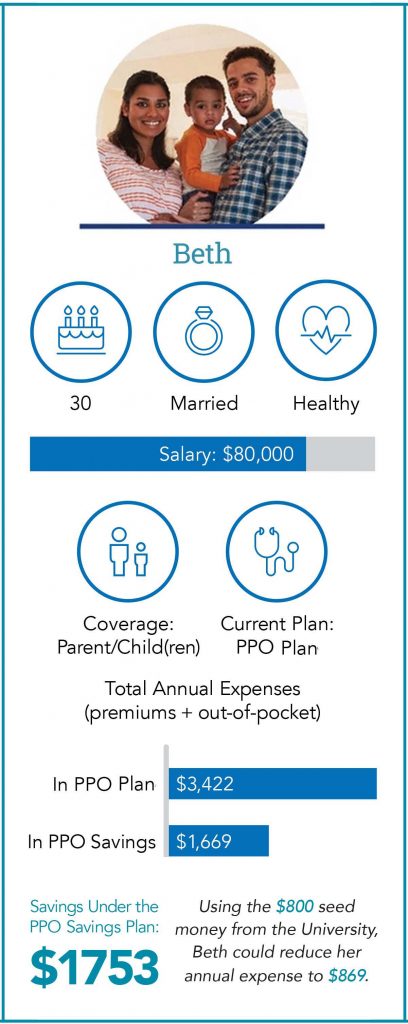

Beth is 30 years old, married with two children, is in good health, and makes $80,000 per year. She covers herself and her children but not her husband because he has coverage through his own employer. She is comfortable with paying more of her up-front medical expenses out-of-pocket for the opportunity to pay lower premiums from her paycheck.

Beth is 30 years old, married with two children, is in good health, and makes $80,000 per year. She covers herself and her children but not her husband because he has coverage through his own employer. She is comfortable with paying more of her up-front medical expenses out-of-pocket for the opportunity to pay lower premiums from her paycheck.

Beth sees a chiropractor and takes prescriptions regularly. Her son has had an annual physical, a primary care physician visit, and two brand prescriptions. Her daughter has had an annual physical, a primary care physician visit, and took three generic prescriptions.

Recommendation after comparison:

The PPO Savings Plan is recommended for Beth. Although Beth spends more for medical services in the PPO Savings Plan versus the PPO Plan, she is paying three times as much in premium for the PPO Plan than in the PPO Savings Plan. Her total expenses (premium contributions plus total out-of-pocket costs) for the year in the PPO Plan are $3,422 vs. $1,669 in the PPO Savings Plan. However, Beth will receive $800 in HSA (health savings account) seed money from the University if she enrolls in the PPO Savings Plan, further reducing her out-of-pocket expenses.